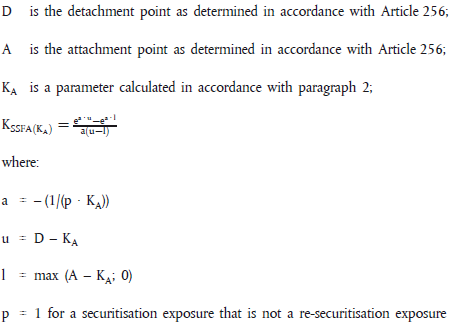

1. Under the SEC-SA, the risk-weighted exposure amount for a position in a securitisation shall be calculated by multiplying the exposure value of the position as calculated in accordance with Article 248 by the applicable risk weight determined as follows, in all cases subject to a floor of 15 %:

2. For the purposes of paragraph 1, KA shall be calculated as follows:

(a) the sum of the nominal amount of underlying exposures in default, to

(b) the sum of the nominal amount of all underlying exposures.

For these purposes, an exposure in default shall mean an underlying exposure which is either: (i) 90 days or more past due; (ii) subject to bankruptcy or insolvency proceedings; (iii) subject to foreclosure or similar proceeding; or (iv) in default in accordance with the securitisation documentation.

Where an institution does not know the delinquency status for 5 % or less of underlying exposures in the pool, the institution may use the SEC-SA subject to the following adj

…