1. Each Member State shall ensure that it is possible to set a systemic risk buffer of Common Equity Tier 1 capital for the financial sector or one or more subsets of that sector on all or a subset of exposures as referred to in paragraph 5 of this Article, in order to prevent and mitigate macroprudential or systemic risks, including macroprudential or systemic risks arising from climate change, not covered by Regulation (EU) No 575/2013 and by Articles 130 and 131 of this Directive, that is to say a risk of disruption in the financial system with the potential to have serious negative consequences for the financial system and the real economy in a specific Member State.

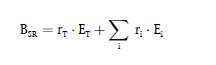

2. Institutions shall calculate the systemic risk buffer as follows:

where:

BSR = the systemic risk buffer;

rT = the buffer rate applicable to the total risk exposure amount of an institution;

ET = the total risk exposure amount of an institution calculated in accordance with Article 92(3) of Regulation (EU) No 575/20

…