120. Amendment of section 81A (further relief from stamp duty in respect of transfers to young trained farmers) of Principal Act.

(1) Section 81A (inserted by the Finance Act 2004) of the Principal Act is amended in subsection (11) by substituting the following for paragraph (a):

"(a) Where any person to whom land was conveyed or transferred by any instrument in respect of which relief from stamp duty under subsection (6) applied -

(i) disposes of such land, or part of such land (in this subsection referred to as a 'part disposal'), within a period of 5 years from the date of execution of that instrument, and

(ii) does not fully expend the proceeds from such disposal, or as the case may be, such part disposal, in acquiring other land within a period of one year from the date of such disposal,

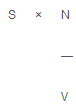

then, such person or, where there is more than one such person, each such person, jointly and severally, shall become liable to pay to the Commissioners a penalty equal to an amount determined by the formula -

where -

S is the amount of stamp duty which would have been charged on that instrument had relief under subsection (6) not applied,

V is the market value of all the land that was conveyed or transferred by the instrument immediately before the disposal, or as the case may be, the part disposal of the land, and

N is the amount of proceeds from the disposal, or as the case may be, the part disposal of the land that was not expended in acquiring other land.