VI. Deduction of investments pursuant to this part

37. Where deductions of investments are made pursuant to this part on scope of application, the deductions will be 50% from Tier 1 and 50% from Tier 2 capital.

38. Goodwill relating to entities subject to a deduction approach pursuant to this part should be deducted from Tier 1 in the same manner as goodwill relating to consolidated subsidiaries, and the remainder of the investments should be deducted as provided for in this part. A similar treatment of goodwill should be applied, if using an alternative group-wide approach pursuant to paragraph 30.

39. The limits on Tier 2 and Tier 3 capital and on innovative Tier 1 instruments will be based on the amount of Tier 1 capital after deduction of goodwill but before the deductions of investments pursuant to this part on scope of application (see Annex 1 for an example how to calculate the 15% limit for innovative Tier 1 instruments).

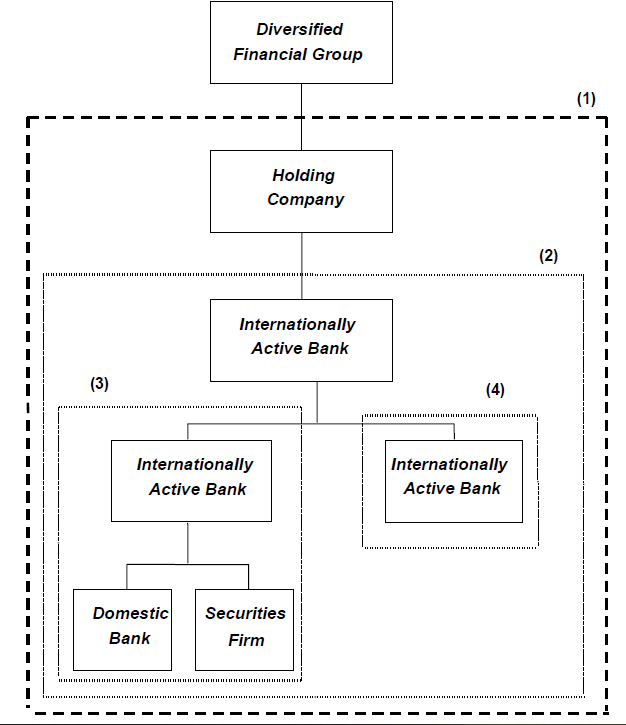

(1) Boundary of predominant banking group. The Framework is to be applied at this level on a consolidated basis, i.e. up to holding company level (paragraph 21).

(2), (3) and (4): the Framework is also to be applied at lower levels to all internationally active banks on a consolidated basis.