4.19 Reporting of margins (paras. 290-315)

290. The collateralisation categories need to be reported in accordance with the Article 5 of the ITS on reporting.

291. The field 'Collateralisation' should be populated based on the agreement and not on the actual collateral exchanged, i.e. if the agreement considers for a two-way initial margin and variation margin, the field should be populated with 'FLCL' even though the current situation might be that no initial margin nor variation margin is exchanged.

292. The table below shows different scenarios of collateralisation and how they should be reported using the categories.

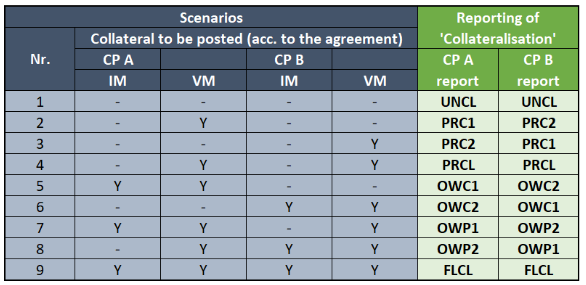

TABLE 18 - COLLATERALISATION CATEGORIES

*UNCL - uncollateralised, PRC1 - Partially collateralised: Counterparty 1, PRC2 - Partially collateralised: Counterparty 2, PRCL - Partially collateralised, OWC1 - One-way collateralised: Counterparty 1 only, OWC2 - One-way collateralised: Counterparty 2 only, OWP1 - One-way/partially collateralised: Counterparty 1, OWP2 - One-way/partially collateralised: Counterparty 2, FLCL - Fully collateralised

293. As specified in Article 4.2 of the RTS on reporting, collateral can be reported on a portfolio basis. This means the reporting of each single executed derivative should not include all the fields related to collateral, to the extent that each single derivative is assigned to a specific portfolio and the relevant information on the portfolio is reported on a daily basis (end-of-day).