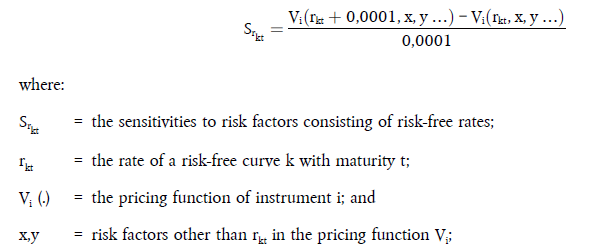

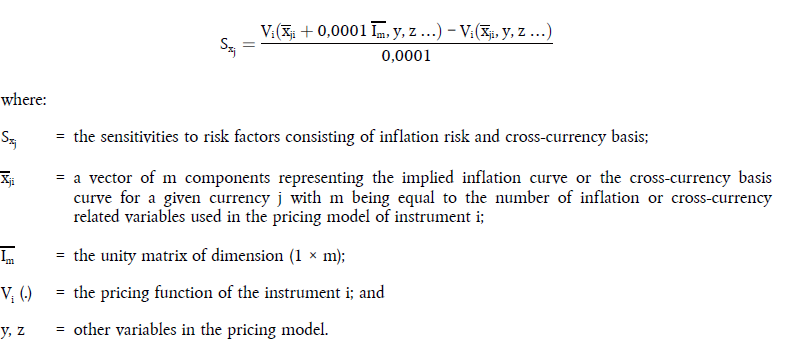

1. Institutions shall calculate delta general interest rate risk (GIRR) sensitivities as follows:

(a) the sensitivities to risk factors consisting of risk-free rates shall be calculated as follows:

(b) the sensitivities to risk factors consisting of inflation risk and cross-currency basis shall be calculated as follows:

2. Institutions shall calculate the delta credit spread risk sensitivities for all securitisation and non-securitisation positions as follows:

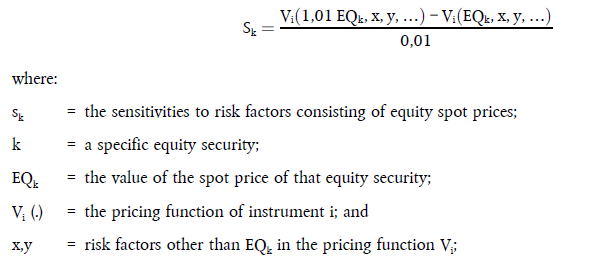

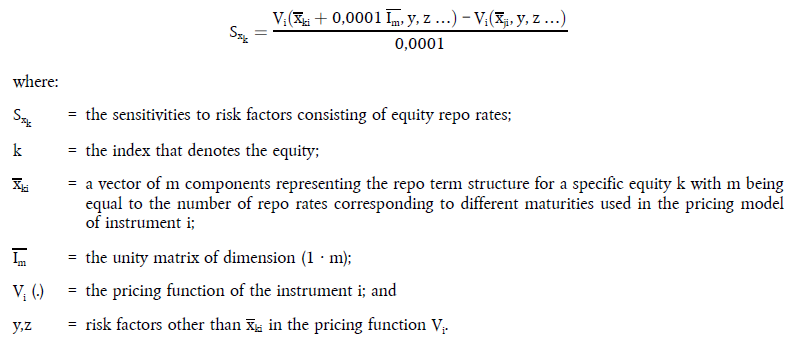

3. Institutions shall calculate delta equity risk sensitivities as follows:

(a) the sensitivities to risk factors consisting of equity spot prices shall be calculated as follows:

(b) the sensitivities to risk factors consisting of equity repo rates shall be calculated as follows:

4. Institutions shall calculate the delta commodity risk sensitivities to each risk factor k as follows:

Vi (.) = the pricing function of instrument i; and

5. Institutions shall calculate the delta foreign exchange risk sensitivities to each forei

…