Table of Contents

Document Overview

LEV20 Calculation (paras. 20.1-20.7) (effective as of 1 January 2023)

This chapter describes how to calculate the leverage ratio.

Version effective as of 01 Jan 2023

Calculation frequency specified for reporting and disclosure purposes. Also takes account of the revised implementation date announced on 27 March 2020.

20.1 The Basel III leverage ratio is intended to:

(1) restrict the build-up of leverage in the banking sector to avoid destabilising deleveraging processes that can damage the broader financial system and the economy; and

(2) reinforce the risk-based capital requirements with a simple, non-risk-based "backstop" measure.

20.2 The Basel Committee is of the view that a simple leverage ratio framework is critical and complementary to the risk-based capital framework and that the leverage should adequately capture both the on- and off-balance sheet sources of banks' leverage.

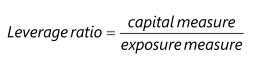

20.3 The leverage ratio is defined as the capital measure (the numerator) divided by the exposure measure (the denominator), with this ratio expressed as a percentage: