Annex VII Part 1 Risk weighted exposure amounts and expected loss amounts

1. CALCULATION OF RISK WEIGHTED EXPOSURE AMOUNTS FOR CREDIT RISK

1. Unless noted otherwise, the input parameters PD, LGD, and maturity value (M) shall be determined as set out in Part 2 and the exposure value shall be determined as set out in Part 3.

2. The risk weighted exposure amount for each exposure shall be calculated in accordance with the following formulae.

1.1. Risk weighted exposure amounts for exposures to corporates, institutions and central governments and central banks.

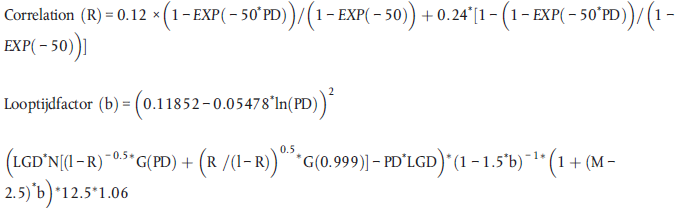

3. Subject to points 5 to 9, the risk weighted exposure amounts for exposures to corporates, institutions and central governments and central banks shall be calculated according to the following formulae:

N(x) denotes the cumulative distribution function for a standard normal random variable (i.e. the probability that a normal random variable with mean zero and variance of one is less than or equal to x). G(Z) denotes the inverse cumulative distribution function for a standard normal random variable (i.e. the value x such that N(x) z)

For PD = 0, RW shall be 0.

For PD = 1: