Version date: 23 October 2023 - onwards

4.2.1 Swaption on a fixed-to-floating IRS (para. 414)

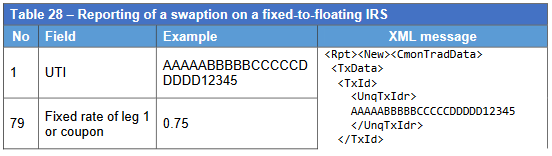

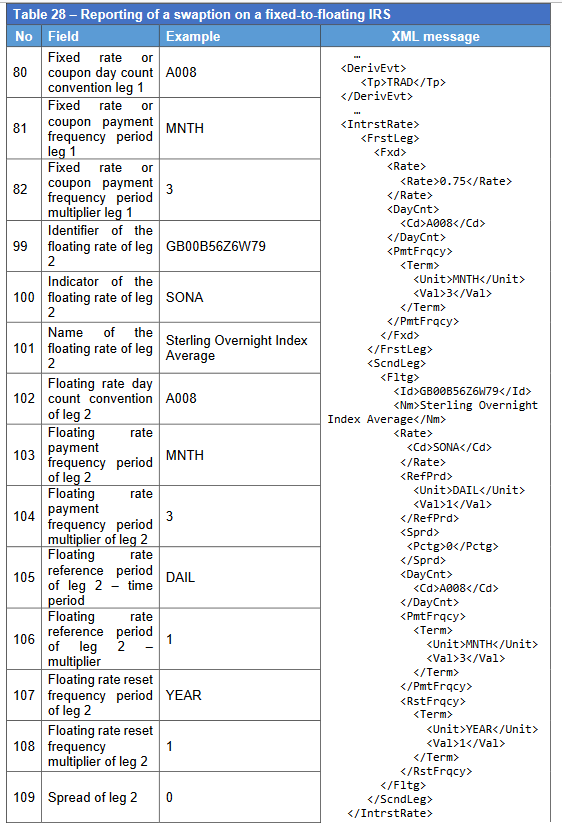

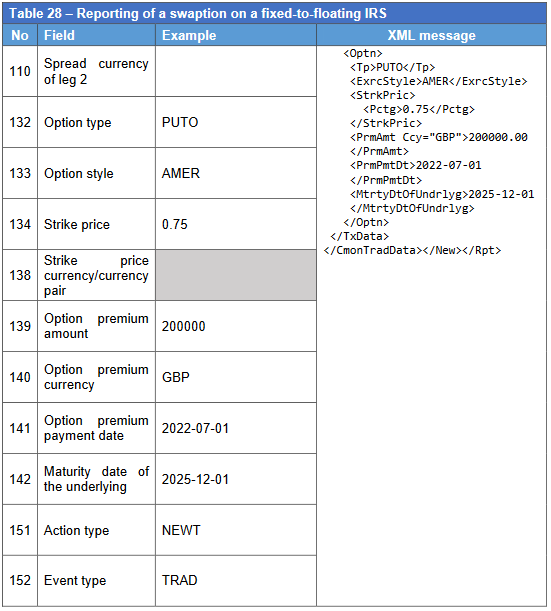

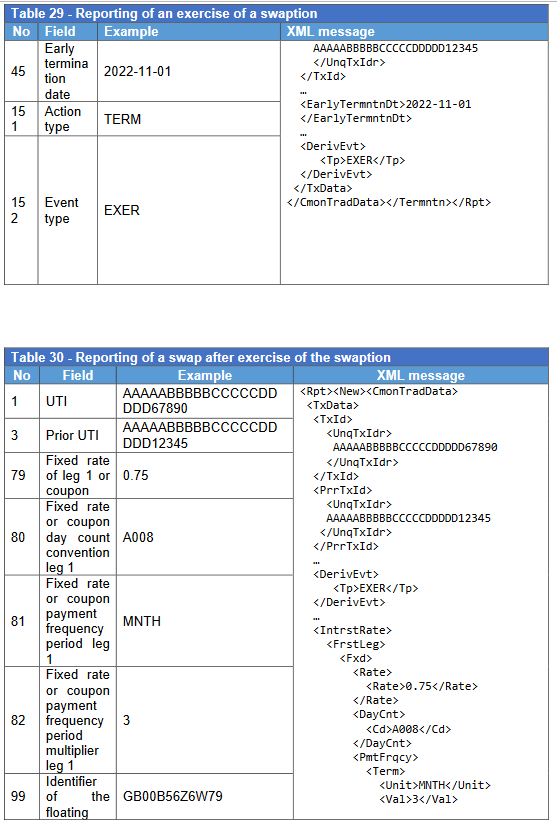

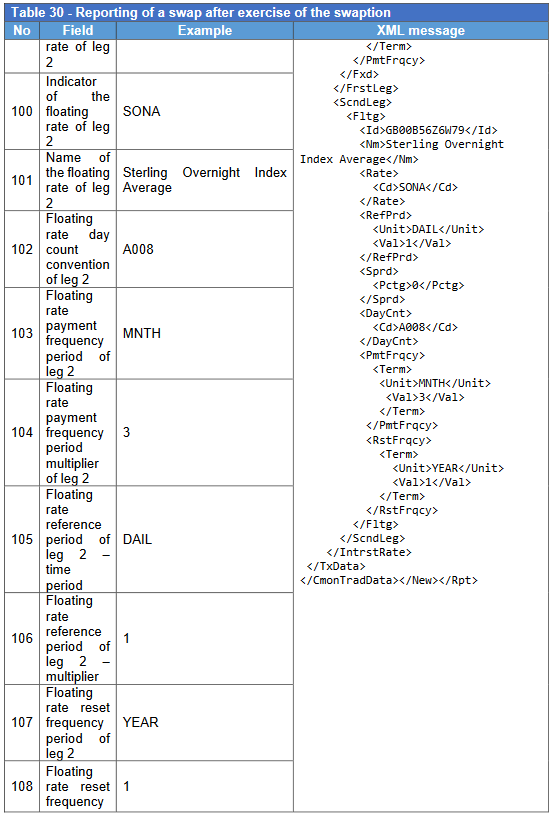

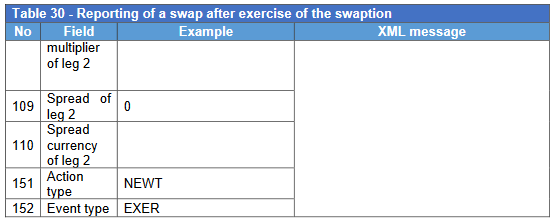

414. Counterparty enters into an American put option on a fixed-to-floating IRS based on 1D SONIA vs 0.75% (with no additional spread). The premium is 200,000 GBP. If exercised, the reporting counterparty will pay fixed rate and the counterparties will exchange payments each 3 months and reset frequency is set to annual. The day count convention is Actual/Actual ISDA.