Table of Contents

Regulation 2015/35/EU - Solvency II Delegated RegulationRecitalsTitle I Valuation and risk-based capital requirements (pillar I), enhanced governance (pillar II) and increased transparency (pillar III) (arts. 1-327)Chapter I General provisions (arts. 1-6)Section 1 Definitions and general principles (arts. 1-2)Article 1 DefinitionsArticle 2 Expert judgementSection 2 External credit assessments (arts. 3-6)Article 3 Association of credit assessments to credit quality stepsArticle 4 General requirements on the use of credit assessmentsArticle 5 Issuers and issue credit assessmentArticle 6 Double credit rating for securitisation positionsChapter II Valuation of assets and liabilities (arts. 7-16)Article 7 Valuation assumptionsArticle 8 ScopeArticle 9 Valuation methodology - general principlesArticle 10 Valuation methodology - valuation hierarchyArticle 11 Recognition of contingent liabilitiesArticle 12 Valuation methods for goodwill and intangible assetsArticle 13 Valuation methods for related undertakingsArticle 14 Valuation methods for specific liabilitiesArticle 15 Deferred taxesArticle 16 Exclusion of valuation methodsChapter III Rules relating to technical provisions (arts. 17-61)Section 1 General provisions (arts. 17-18)Article 17 Recognition and derecognition of insurance and reinsurance obligationsArticle 18 Boundary of an insurance or reinsurance contractSection 2 Data quality (arts. 19-21)Article 19 Data used in the calculation of technical provisionsArticle 20 Limitations of dataArticle 21 Appropriate use of approximations to calculate the best estimateSection 3 Methodologies to calculate technical provisions (arts. 22-42)Subsection 1 Assumptions underlying the calculation of technical provisions (arts. 22-26)Article 22 General provisionsArticle 23 Future management actionsArticle 24 Future discretionary benefitsArticle 25 Separate calculation of the future discretionary benefitsArticle 26 Policyholder behaviourSubsection 2 Information underlying the calculation of best estimates (art. 27)Article 27 Credibility of informationSubsection 3 Cash flow projections for the calculation of the best estimate (arts. 28-36)Article 28 Cash flowsArticle 29 Expected future developments in the external environmentArticle 30 Uncertainty of cash flowsArticle 31 ExpensesArticle 32 Contractual options and financial guaranteesArticle 33 Currency of the obligationArticle 34 Calculation methodsArticle 35 Homogeneous risk groups of life insurance obligationsArticle 36 Non-life insurance obligationsSubsection 4 Risk margin (arts. 37-39)Article 37 Calculation of the risk marginArticle 38 Reference undertakingArticle 39 Cost-of-Capital rateSubsection 5 Calculation of technical provisions as a whole (art. 40)Article 40 Circumstances in which technical provisions shall be calculated as a whole and the method to be usedSubsection 6 Recoverables from reinsurance contracts and special purpose vehicles (arts. 41-42)Article 41 General provisionsArticle 42 Counterparty default adjustmentSection 4 Relevant risk-free interest rate term structure (arts. 43-54)Subsection 1 General provisions (art. 43)Article 43 General provisionsSubsection 2 Basic risk free interest rate term structure (arts. 44-48)Article 44 Relevant financial instruments to derive the basic risk-free interest ratesArticle 45 Adjustment to swap rates for credit riskArticle 46 ExtrapolationArticle 47 Ultimate forward rateArticle 48 Basic risk-free interest rate term structure of currencies pegged to the euroSubsection 3 Volatility adjustment (arts. 49-51)Article 49 Reference portfoliosArticle 50 Formula to calculate the spread underlying the volatility adjustmentArticle 51 Risk-corrected spreadSubsection 4 Matching adjustment (arts. 52-54)Article 52 Mortality risk stressArticle 53 Calculation of the matching adjustmentArticle 54 Calculation of the fundamental spreadSection 5 Lines of business (art. 55)Article 55 Lines of businessSection 6 Proportionality and simplifications (arts. 56-61)Article 56 ProportionalityArticle 57 Simplified calculation of recoverables from reinsurance contracts and special purpose vehiclesArticle 58 Simplified calculation of the risk marginArticle 59 Calculations of the risk margin during the financial yearArticle 60 Simplified calculation of the best estimate for insurance obligations with premium adjustment mechanismArticle 61 Simplified calculation of the counterparty default adjustmentChapter IV Own funds (arts. 62-82)Section 1 Determination of own funds (arts. 62-68)Subsection 1 Supervisory approval of ancillary own funds (arts. 62-67)Article 62 Assessment of the applicationArticle 63 Assessment of the application - Status of the counterpartiesArticle 64 Assessment of the application - Recoverability of the fundsArticle 65 Assessment of the application - Information on the outcome of past callsArticle 66 Specification of amount relating to an unlimited amount of ancillary own fundsArticle 67 Specification of amount and timing relating to the approval of a methodSubsection 2 Own funds treatment of participations (s. 68)Article 68 Treatment of participations in the determination of basic own fundsSection 2 Classification of own funds (arts. 69-79)Article 69 Tier 1 - List of own-fund itemsArticle 70 Reconciliation ReserveArticle 71 Tier 1 - Features determining classificationArticle 72 Tier 2 Basic own-funds - List of own-fund itemsArticle 73 Tier 2 Basic own-funds - Features determining classificationArticle 74 Tier 2 Ancillary own-funds - List of own-fund itemsArticle 75 Tier 2 Ancillary own-funds - Features determining classificationArticle 76 Tier 3 Basic own-funds - List of own-fund itemsArticle 77 Tier 3 Basic own-funds - Features determining classificationArticle 78 Tier 3 Ancillary own-funds - List of own-funds itemsArticle 79 Supervisory Authorities approval of the assessment and classification of own-fund itemsSection 3 Eligibility of own funds (arts. 80-82)Subsection 1 Ring-fenced funds (arts. 80-81)Article 80 Ring-fenced funds requiring adjustmentsArticle 81 Adjustment for ring-fenced funds and matching adjustment portfoliosSubsection 2 Quantitative limits (art. 82)Article 82 Eligibility and limits applicable to Tiers 1, 2 and 3Chapter V Solvency Capital Requirement Standard Formula (arts. 83-221)Section 1 General provisions (arts. 83-113)Subsection 1 Scenario based calculations (art. 83)Article 83Subsection 2 Look-through approach (art. 84)Article 84Subsection 3 Regional governments and local authorities (art. 85)Article 85Subsection 4 Material basis risk (art. 86)Article 86Subsection 5 Calculation of the basic solvency capital requirement (art. 87)Article 87Subsection 6 Proportionality and simplifications (arts. 88-112b)Article 88 ProportionalityArticle 89 General provisions for simplifications for captivesArticle 90 Simplified calculation for captive insurance and reinsurance undertakings of the capital requirement for non-life premium and reserve riskArticle 90a Simplified calculation for discontinuance of insurance policies in the non-life lapse risk sub-moduleArticle 90b Simplified calculation of the sum insured for natural catastrophe risksArticle 90c Simplified calculation of the capital requirement for fire riskArticle 91 Simplified calculation of the capital requirement for life mortality riskArticle 92 Simplified calculation of the capital requirement for life longevity riskArticle 93 Simplified calculation of the capital requirement for life disability-morbidity riskArticle 94 Simplified calculation of the capital requirement for life-expense riskArticle 95 Simplified calculation of the capital requirement for permanent changes in lapse ratesArticle 95a Simplified calculation of the capital requirement for risks in the life lapse risk sub-moduleArticle 96 Simplified calculation of the capital requirement for life-catastrophe riskArticle 96a Simplified calculation for discontinuance of insurance policies in the NSLT health lapse risk sub-moduleArticle 97 Simplified calculation of the capital requirement for health mortality riskArticle 98 Simplified calculation of the capital requirement for health longevity riskArticle 99 Simplified calculation of the capital requirement for medical expense disability-morbidity riskArticle 100 Simplified calculation of the capital requirement for income protection disability-morbidity riskArticle 101 Simplified calculation of the capital requirement for health expense riskArticle 102 Simplified calculation of the capital requirement for SLT health lapse riskArticle 102a Simplified calculation of the capital requirement for risks in the SLT health lapse risk sub-moduleArticle 103 Simplified calculation of the capital requirement for interest rate risk for captive insurance or reinsurance undertakingsArticle 104 Simplified calculation for spread risk on bonds and loansArticle 105 Simplified calculation for captive insurance or reinsurance undertakings of the capital requirement for spread risk on bonds and loansArticle 105a Simplified calculation for the risk factor in the spread risk sub-module and the market risk concentration sub-moduleArticle 106 Simplified calculation of the capital requirement for market risk concentration for captive insurance or reinsurance undertakingsArticle 107 Simplified calculation of the risk mitigating effect for reinsurance arrangements or securitisationArticle 108 Simplified calculation of the risk mitigating effect for proportional reinsurance arrangementsArticle 109 Simplified calculations for pooling arrangementsArticle 110 Simplified calculation - grouping of single name exposuresArticle 111 Simplified calculation of the risk mitigating effectArticle 111a Simplified calculation of the risk-mitigating effect on underwriting riskArticle 112 Simplified calculation of the risk adjusted value of collateral to take into account the economic effect of the collateralArticle 112a Simplified calculation of the loss-given-default for reinsuranceArticle 112b Simplified calculation of the capital requirement for counterparty default risk on type 1 exposuresSubsection 7 Scope of the under writing risk modules (art. 113)Article 113Section 2 Non-life underwriting risk module (arts. 114-135)Article 114 Non-life underwriting risk moduleArticle 115 Non-life premium and reserve risk sub-moduleArticle 116 Volume measure for non-life premium and reserve riskArticle 117 Standard deviation for non-life premium and reserve riskArticle 118 Non-life lapse risk sub-moduleArticle 119 Non-life catastrophe risk sub-moduleArticle 120 Natural catastrophe risk sub-moduleArticle 121 Windstorm risk sub-moduleArticle 122 Earthquake risk sub-moduleArticle 123 Flood risk sub-moduleArticle 124 Hail risk sub-moduleArticle 125 Subsidence risk sub-moduleArticle 126 Interpretation of catastrophe scenariosArticle 127 Sub-module for catastrophe risk of non-proportional property reinsuranceArticle 128 Man-made catastrophe risk sub-moduleArticle 129 Motor vehicle liability risk sub-moduleArticle 130 Marine risk sub-moduleArticle 131 Aviation risk sub-moduleArticle 132 Fire risk sub-moduleArticle 133 Liability risk sub-moduleArticle 134 Credit and suretyship risk sub-moduleArticle 135 Sub-module for other non-life catastrophe riskSection 3 Life underwriting risk module (arts. 136-143)Article 136 Correlation coefficientsArticle 137 Mortality risk sub-moduleArticle 138 Longevity risk sub-moduleArticle 139 Disability-morbidity risk sub-moduleArticle 140 Life-expense risk sub-moduleArticle 141 Revision risk sub-moduleArticle 142 Lapse risk sub-moduleArticle 143 Life-catastrophe risk sub-moduleSection 4 Health underwriting risk module (arts. 144-163)Article 144 Health underwriting risk moduleArticle 145 NSLT health underwriting risk sub-moduleArticle 146 NSLT health premium and reserve risk sub-moduleArticle 147 Volume measure for NSLT health premium and reserve riskArticle 148 Standard deviation for NSLT health premium and reserve riskArticle 149 Health risk equalisation systemsArticle 150 NSLT health lapse risk sub-moduleArticle 151 SLT health underwriting risk sub-moduleArticle 152 Health mortality risk sub-moduleArticle 153 Health longevity risk sub-moduleArticle 154 Health disability-morbidity risk sub-moduleArticle 155 Capital requirement for medical expense disability-morbidity riskArticle 156 Capital requirement for income protection disability-morbidity riskArticle 157 Health expense risk sub-moduleArticle 158 Health revision risk sub-moduleArticle 159 SLT health lapse risk sub-moduleArticle 160 Health catastrophe risk sub-moduleArticle 161 Mass accident risk sub-moduleArticle 162 Accident concentration risk sub-moduleArticle 163 Pandemic risk sub-moduleSection 5 Market risk module (arts. 164-188)Subsection 1 Correlation coefficients (art. 164)Article 164Subsection 1a Qualifying infrastructure investments (arts. 164a-164b)Article 164a Qualifying infrastructure investmentsArticle 164b Qualifying infrastructure corporate investmentsSubsection 2 Interest rate risk sub-module (arts. 165-167)Article 165 General provisionsArticle 166 Increase in the term structure of interest ratesArticle 167 Decrease in the term structure of interest ratesSubsection 3 Equity risk sub-module (arts. 168-173)Article 168 General provisionsArticle 168a Qualifying unlisted equity portfoliosArticle 169 Standard equity risk sub-moduleArticle 170 Duration-based equity risk sub-moduleArticle 171 Strategic equity investmentsArticle 171a Long-term equity investmentsArticle 172 Symmetric adjustment of the equity capital chargeArticle 173 Criteria for the use of transitional measure for standard equity riskSubsection 4 Proper ty risk sub-module (art. 174)Article 174Subsection 5 Spread risk sub-module (arts. 175-181)Article 175 Scope of the spread risk sub-moduleArticle 176 Spread risk on bonds and loansArticle 176a Internal assessment of credit quality steps of bonds and loansArticle 176b Requirements for an undertaking's own internal credit assessment of bonds and loansArticle 176c Assessment of credit quality steps of bonds and loans based on an approved internal modelArticle 177 Spread risk on securitisation positions: general provisionsArticle 178 Spread risk on securitisation positions: calculation of the capital requirementArticle 178a Spread risk on securitisation positions: transitional provisionsArticle 179 Spread risk on credit derivativesArticle 180 Specific exposuresArticle 181 Application of the spread risk scenarios to matching adjustment portfoliosSubsection 6 Market risk concentrations sub-module (arts. 182-187)Article 182 Single name exposureArticle 183 Calculation of the capital requirement for market risk concentrationArticle 184 Excess exposureArticle 185 Relative excess exposure thresholdsArticle 186 Risk factor for market risk concentrationArticle 187 Specific exposuresSubsection 7 Currency risk sub-module (art. 188)Article 188Section 6 Counterparty default risk module (arts. 189-202)Subsection 1 General provisions (arts. 189-198)Article 189 ScopeArticle 190 Single name exposuresArticle 191 Mortgage loansArticle 192 Loss-given-defaultArticle 192a Exposure to clearing membersArticle 193 Loss-given-default for pool exposures of type AArticle 194 Loss-given-default for pool exposures of type BArticle 195 Loss-given-default for pool exposures of type CArticle 196 Risk-mitigating effectArticle 197 Risk-adjusted value of collateralArticle 198 Risk-adjusted value of mortgageSubsection 2 Type 1 exposures (arts. 199-201)Article 199 Probability of defaultArticle 200 Type 1 exposuresArticle 201 Variance of the loss distribution of type 1 exposuresSubsection 3 Type 2 exposures (art. 202)Article 202 Type 2 exposuresSection 7 Intangible asset module (arts. 203)Article 203Section 8 Operational risk (art. 204)Article 204Section 9 Adjustment for the loss-absorbing capacity of technical provisions and deferred taxes (arts. 205-207)Article 205 General provisionsArticle 206 Adjustment for the loss-absorbing capacity of technical provisionsArticle 207 Adjustment for the loss-absorbing capacity of deferred taxesSection 10 Risk mitigation techniques (arts. 208-215)Article 208 Methods and AssumptionsArticle 209 Qualitative CriteriaArticle 210 Effective Transfer of RiskArticle 211 Risk-Mitigation techniques using reinsurance contracts or special purpose vehiclesArticle 212 Financial Risk-Mitigation techniquesArticle 213 Status of the counterpartiesArticle 214 Collateral ArrangementsArticle 215 GuaranteesSection 11 Ring fenced funds (arts. 216-217)Article 216 Calculation of the Solvency Capital Requirement in the case of ring-fenced funds and matching adjustment portfoliosArticle 217 Solvency Capital Requirement calculation method for ring-fenced funds and matching adjustment portfoliosSection 12 Undertaking-specific parameters (arts. 218-220)Article 218 Subset of standard parameters that may be replaced by undertaking-specific parametersArticle 219 Data criteriaArticle 220 Standardised methods to calculate the undertaking-specific parametersSection 13 Procedure for updating correlation parameters (art. 221)Article 221Chapter VI Solvency capital requirement - full and partial internal models (arts. 222-247)Section 1 Definitions (art. 222)Article 222 MaterialitySection 2 Use test (arts. 223-227)Article 223 Use of the internal modelArticle 224 Fit to the businessArticle 225 Understanding of the internal modelArticle 226 Support of decision-making and integration with risk managementArticle 227 Simplified calculationSection 3 Statistical quality standards (arts. 228-237)Article 228 Probability distribution forecastArticle 229 Adequate, applicable and relevant actuarial techniquesArticle 230 Information and assumptions used for the calculation of the probability distribution forecastArticle 231 Data used in the internal modelArticle 232 Ability to rank riskArticle 233 Coverage of all material risksArticle 234 Diversification effectsArticle 235 Risk-mitigation techniquesArticle 236 Future management actionsArticle 237 Understanding of external models and dataSection 4 Calibration standards (art. 238)Article 238Section 5 Integration of partial internal models (art. 239)Article 239Section 6 Profit and loss attribution (art. 240)Article 240Section 7 Validation standards (arts. 241-242)Article 241 Model validation processArticle 242 Validation toolsSection 8 Documentation standards (arts. 243-246)Article 243 General provisionsArticle 244 Minimum content of the documentationArticle 245 Circumstances under which the internal model does not work effectivelyArticle 246 Changes to the internal modelSection 9 External models and data (art. 247)Article 247Chapter VII Minimum capital requirement (arts. 248-253)Article 248 Minimum Capital RequirementArticle 249 Linear Minimum Capital RequirementArticle 250 Linear formula component for non-life insurance and reinsurance obligationsArticle 251 Linear formula component for life insurance and reinsurance obligationsArticle 252 Minimum Capital Requirement: composite insurance undertakingsArticle 253 Absolute floor of the Minimum Capital RequirementChapter VIII Investment in securitisation positions (arts. 254-257)Article 254 Risk retention requirements relating to the originators, sponsors or original lendersArticle 255 Exemptions to risk retention requirementsArticle 256 Qualitative requirements relating to insurance and reinsurance undertakingsArticle 257 Requirements for investments in securitisation that no longer comply with the risk-retention and qualitative requirementsChapter IX System of governance (arts. 258-275a)Section 1 Elements of the system of governance (arts. 258-267)Article 258 General governance requirementsArticle 259 Risk Management SystemArticle 260 Risk management areasArticle 261 Risk management in undertakings providing loans and/or mortgage insurance or reinsuranceArticle 261a Risk management for qualifying infrastructure investments or qualifying infrastructure corporate investmentsArticle 262 Overall solvency needsArticle 263 Alternative methods for valuationArticle 264 Valuation of technical provisions - validationArticle 265 Valuation of technical provisions - documentationArticle 266 Internal control systemArticle 267 Internal control of valuation of assets and liabilitiesSection 2 Functions (arts. 268-272)Article 268 Specific provisionsArticle 269 Risk management functionArticle 270 Compliance functionArticle 271 Internal audit functionArticle 272 Actuarial functionSection 3 Fit and proper requirements (art. 273)Article 273Section 4 Outsourcing (art. 274)Article 274Section 5 Remuneration policy (art. 275)Article 275Section 6 Investments (art. 275a)Article 275a Integration of sustainability risks in the prudent person principleChapter X Capital add-on (arts. 276-287)Section 1 Circumstances for imposing a capital add-on (arts. 276-281)Article 276 Assessment of a significant deviation as regards the SCRArticle 277 Assessment of a significant deviation as regards the governanceArticle 278 Assessment of a significant deviation as regards adjustments to the relevant risk-free rate and transitional measuresArticle 279 Add-ons in relation to deviations from Solvency Capital Requirement assumptionsArticle 280 Assessment of the requirement to use an internal modelArticle 281 Appropriate timeframe for adapting the internal modelSection 2 Methodologies for calculating capital add-ons (arts. 282-287)Article 282 Calculation of add-ons in relation to deviations from SCR assumptionsArticle 283 Scope and approach of modifications as regards a deviation from SCR assumptionsArticle 284 Calculation of add-ons in relation to adjustments to the relevant risk-free rate or transitional measuresArticle 285 Scope and approach of modifications as regards adjustments to the relevant risk-free rate and transitional measuresArticle 286 Calculation of add-ons in relation to deviations from governance standardsArticle 287 Apportionment of add-ons for undertakings which simultaneously pursue life and non-life insurance activitiesChapter XI Extension of the recovery period (arts. 288-289)Article 288 Assessment of exceptional adverse situationsArticle 289 Factors and criteria to determine the extension of the recovery periodChapter XII Public disclosure (arts. 290-303)Section 1 Solvency and financial condition report: structure and contents (arts. 290-298)Article 290 StructureArticle 291 MaterialityArticle 292 SummaryArticle 293 Business and performanceArticle 294 System of governanceArticle 295 Risk profileArticle 296 Valuation for solvency purposesArticle 297 Capital managementArticle 298 Additional voluntary informationSection 2 Solvency and financial condition report: non-disclosure of information (art. 299)Article 299Section 3 Solvency and financial condition report: deadlines, means of disclosure and updates (arts. 300-303)Article 300 DeadlinesArticle 301 Means of disclosureArticle 302 UpdatesArticle 303 Transitional arrangements on comparative informationChapter XIII Regular supervisory reporting (arts. 304-314)Section 1 Elements and contents (arts. 304-311)Article 304 Elements of the regular supervisory reportingArticle 305 MaterialityArticle 306 Own-risk and solvency assessment supervisory reportArticle 307 Business and performanceArticle 308 System of governanceArticle 309 Risk profileArticle 310 Valuation for solvency purposesArticle 311 Capital managementSection 2 Deadlines and means of communication (arts. 312-314)Article 312 DeadlinesArticle 313 Means of communicationArticle 314 Transitional information requirementsChapter XIV Transparency and accountability of supervisory Authorities (arts. 315-317)Article 315 Confidential informationArticle 316 Aggregate statistical dataArticle 317 Means of disclosureChapter XV Special puropose vehicles (arts. 318-327)Section 1 Authorization (art. 318)Article 318Section 2 Mandatory contract conditions (arts. 319-321)Article 319 Fully FundedArticle 320 Effective transfer of riskArticle 321 Rights of the providers of debt or financing mechanismsSection 3 System of governance (arts. 322-324)Article 322 Fit and proper requirements of persons who effectively run a special purpose vehicleArticle 323 Fit and proper requirements for shareholders or members with a qualifying holdingArticle 324 Sound administrative and accounting procedures, adequate internal control mechanisms and risk-management requirementsSection 4 Supervisory reporting (art. 325)Article 325 Supervisory reportingSection 5 Solvency requirements (arts. 326-327)Article 326 Solvency requirementsArticle 327 Solvency requirements on investmentsTitle II Insurance groups (arts. 328-377)Chapter I Solvency calculation at group level (arts. 328-342)Section 1 Group solvency: choice of calculation method and general principles (arts. 328-330)Article 328 Choice of methodArticle 329 Treatment of specific related undertakingsArticle 330 Availability at group level of the eligible own funds of related undertakingsSection 2 Group solvency: calculation methods (arts. 331-342)Article 331 Classification of own-fund items of related insurance and reinsurance undertakings at group levelArticle 332 Classification of own-fund items of related third-country insurance or reinsurance undertakings at group levelArticle 333 Classification of own-fund items of insurance holding companies, mixed financial holding companies, and subsidiary ancillary services undertakings at group levelArticle 334 Classification of own-fund items of residual related undertakingsArticle 335 Method 1: determination of consolidated dataArticle 336 Method 1: Calculation of the consolidated group Solvency Capital RequirementArticle 337 Method 1: determination of the local currency for the purposes of the currency risk calculationArticle 338 Method 1: group-specific parametersArticle 339 Method 1: best estimateArticle 340 Method 1: Risk marginArticle 341 Combination of methods 1 and 2: minimum consolidated group Solvency Capital RequirementArticle 342 Method 2: Elimination of intra-group creation of capital in relation to the best estimateChapter II Internal models for the calculation of the consolidated group Solvency Capital Requirement (arts. 343-350)Section 1 Full and partial internal models used to calculate only the group solvency capital requirement (arts. 343-346)Article 343 Application for the use of an internal model to calculate only the consolidated group Solvency Capital RequirementArticle 344 Assessment of the application for the use of an internal model to calculate only the consolidated group Solvency Capital RequirementArticle 345 Decision on the application and transitional plan to extend the scope of a partial internal model used to calculate only the consolidated group Solvency Capital RequirementArticle 346 Use test for internal models used to calculate only the consolidated group Solvency Capital RequirementSection 2 Use of a group internal model (arts. 347-350)Article 347 Application to use a group internal modelArticle 348 Assessment of the completeness of an application to use a group internal modelArticle 349 Joint decision on the application and transitional plan to extend the scope of the modelArticle 350 Use test for group internal modelsChapter III Supervision of group solvency for groups with centralised risk management (arts. 351-353)Article 351 Assessment of conditions: criteriaArticle 352 Assessment of conditions: proceduresArticle 353 Assessment of an emergency situation: criteriaChapter IV Coordination of group supervision (arts. 354-358)Section 1 Colleges of supervisors (arts. 354-356)Article 354 Participation of supervisors of significant branches and related undertakingsArticle 355 Coordination arrangementsArticle 356 Supervisory approval of group-specific parametersSection 2 Exchange of information (art. 357)Article 357 Information to be exchanged on a systematic basisSection 3 National or regional subgroup supervision (art. 358)Article 358Chapter V Public disclosure (arts. 359-371)Section 1 Group solvency and financial condition report (arts. 359-364)Article 359 Structure and contentsArticle 360 LanguagesArticle 361 Non-disclosure of informationArticle 362 DeadlinesArticle 363 UpdatesArticle 364 Transitional arrangements on comparative informationSection 2 Single solvency and financial condition report (arts. 365-371)Article 365 Structure and contentsArticle 366 LanguagesArticle 367 Non-disclosure of informationArticle 368 DeadlinesArticle 369 UpdatesArticle 370 ReferenceArticle 371 Transitional arrangements on comparative informationChapter VI Group supervisory reporting (arts. 372-377)Section 1 Regular reporting (arts. 372-375)Article 372 Elements and contentsArticle 373 DeadlinesArticle 374 LanguagesArticle 375 Additional transitional information on groupsSection 2 Reporting on risk concentrations and intragroup transactions (arts. 376-377)Article 376 Significant risk concentrations (definition, identification and thresholds)Article 377 Significant intragroup transactions (definition, identification)Title III Third country eequivalence and final provisions (arts. 378-381)Chapter I Undertakings carrying out reinsurance activities with their head office in a third country (art. 378)Article 378 Criteria for assessing third country equivalenceChapter II Related third country insurance and reinsurance undertakings (art. 379)Article 379 Criteria for assessing third country equivalenceChapter III Insurance and reinsurance undertakings with the parent undertakings outside the Union (art. 380)Article 380 Criteria for assessing third country equivalenceChapter IV Final provisions (art. 381)Article 381Annex I Lines of businessAnnex II Segmentation of non-life insurance and reinsurance obligations and standard deviations for the non-life premium and reserve risk sub-moduleAnnex III Factor for geographical diversification of premium and reserve riskAnnex IV Correlation matrix for non-life premium and reserve riskAnnex V Parameters for the Windstorm risk sub-moduleAnnex VI Parameters for the earthquake risk sub-moduleAnnex VII Parameters for the flood risk sub-moduleAnnex VIII Parameters for the hail risk sub-moduleAnnex IX The geographical division of regions set out in Annexex V-VIII into risk zonesAnnex X Risk weights for catastrophe risk zonesAnnex XI Liability risk groups, risk factors and correlation coefficients for the liability risk sub-moduleAnnex XII Groups of obligations and risk factors for the sub-module for other non-life catastrophe riskAnnex XIII List of regions for which natural catastrophe risk is not calculated based on premiumsAnnex XIV Segmentation of NSLT health insurance and reinsurance obligations and standard deviations for the NSLT health premium and reserve risk sub-moduleAnnex XV Correlation matrix for NSLT health premium and reserve riskAnnex XVI Health catastrophe risk sub-module of the Solvency Capital Requirement standard formulaAnnex XVII Method-specific data requirements and method specifications for undertaking-specific parameters of the standard formulaAnnex XVIII Intergration techniques for partial internal modelsAnnex XIX MCR risk factors for non-life and health insurance or reinsurance obligationsAnnex XX Structure of the solvency and financial condition report and regular Supervisory reportAnnex XXI Aggregate statistical dataAnnex XXII Correlation coefficients for windstorm riskAnnex XXIII Correlation coefficients for earthquake riskAnnex XXIV Correlation coefficients for flood riskAnnex XXV Correlation coefficients for hail riskAnnex XXVI Correlation coefficients for subsidence riskDone at

Document Overview

Tools

Print / Export

Notification

Bookmark

Share / Source link

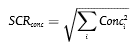

Article 183 Calculation of the capital requirement for market risk concentration

1. The capital requirement for market risk concentration shall be equal to the following:

where:

(a) the sum covers all single name exposures i;

(b) Conci denotes the capital requirement for market risk concentration on a single name exposure i.

2. For each single name exposure i, the capital requirement for market risk concentration Conci shall be equal to the loss in the basic own funds that would result from an instantaneous decrease in the value of the assets corresponding to the single name exposure i equal to the following:

XSi • gi

where:

(a) XSi is the excess exposure referred to in Article 184;

(b) gi is the risk factor for market risk concentration referred to in Articles 186 and 187;