1. Net JTD amounts shall be multiplied by:

(a) for tranched products, the default risk weights corresponding to their credit quality as specified in Article 325y(1) and (2);

(b) for non-tranched products, the default risk weights referred to in Article 325aa(1).

2. Risk-weighted net JTD amounts shall be assigned to buckets that correspond to an index.

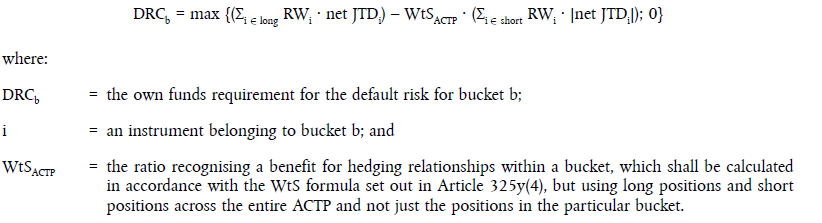

3. Weighted net JTD amounts shall be aggregated within each bucket in accordance with the following formula:

4. Institutions shall calculate the own funds requirements for the default risk for the ACTP by using the following formula: