1. Between vega risk sensitivities within the same bucket of the general interest rate risk (GIRR) class, the correlation parameter ρkl shall be set as follows:

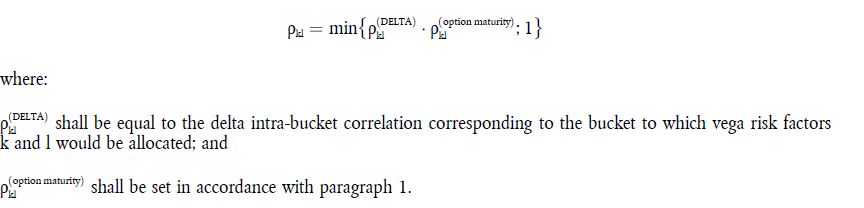

2. Between vega risk sensitivities within a bucket of the other risk classes, the correlation parameter ρkl shall be set as follows:

3. With regard to vega risk sensitivities between buckets within a risk class (GIRR and non-GIRR), the same correlation parameters for γbc, as specified for delta correlations for each risk class in Section 4, shall be used in the vega risk context.

4. There shall be no diversification or hedging benefit recognised in the standardised approach between vega risk factors and delta risk factors. Vega risk charges and delta risk charges shall be aggregated by simple summation.

5. The curvature risk correlations shall be the square of corresponding delta risk correlations ρkl and γbc referred to in Subsection 1.